History of Money: The History of Money, Fiat Currency, Gold & Banking

Learn the history of money from ancient accounting and metal coinage to banking, paper money, fiat currency, the gold standard, Bretton Woods, and modern digital money.

The History of the Creation of Money

Have you ever wondered how it came to be that pieces of cotton paper and numbers on a screen managed to dominate society and consumed the desires of most people? The evolution of money is a long and complicated story and this article intends to only cover the bare essentials. For those interested in learning more, The Ascent of Money by Niall Ferguson is a good place to start.

The common story goes that money arose to fix the shortcomings of barter and serve as a medium of exchange. Although this makes sense, there is no actual proof to support this myth. In the oldest clay tablets uncovered by archaeologists, a concept of money appears alongside the earliest known writing. Albeit, rudimentary writing. Therefore, it can be argued that there is no written record of the emergence of money as a phenomenon. The oldest confirmed proto-cuneiform text is the 5,5500-year-old Kish Tablet, still without a direct translation. Scholars generally agree that proto-cuneiform originated primarily as a system for economic accounting. Only later advancements in cuneiform led to an attempt to correspond written text with an actual spoken language[1]. The significance of this should not be understated, as it seems that the very foundations of writing began with a need to log economic activities. Even thousands of years ago, people were still obsessed with keeping track of commerce, even if it just existed in the form of grain, services, or religious donations.

The Kish Tablet

From the tablets that can actually be translated, the earliest transactions were recorded by religious leaders in Sumeria, tracking who donated what and how much to the temple. A rudimentary form of bookkeeping was used, which evolved over the course of centuries. The kings of Babylon (1600-1800 B.C.) began creating clay tokens that gave bearers the right to a set amount of grain at harvest time, or a set amount of silver after a journey was completed. Systems of debt must have existed by this point in time. In the Code of Hammurabi (roughly 1755 B.C.), one of the most well-known ancient legal codes, debt forgiveness was mandated every three years[2]. The use of silver (initially as a weight) shekels is also attested to. This is all to say that economic activity was a core feature of life at the dawn of human civilization.

The next major advancement in money occurred in ancient Lydia around 600 B.C. This civilization, located off the coast of western Anatolia in what is now Turkey, introduced the first true coinage. The Lydians were the first known civilization to create coins out of a mixture of silver and gold known as electrum[3]. Gold and silver were already prized across many ancient civilizations, usually as jewelry for the ruling elite or in the form of weights in Mesopotamia. The Varna Necropolis, for example, featured elaborate gold ornaments dating back to 4200 B.C[4]. Given this long-standing value, the Lydians’ use of precious metals in coinage spread fast.

Several factors contributed to the rapid spread of precious-metal coinage: availability, durability, portability, reliability, and broad appeal. The Athenians adopted coinage and standardized their own silver tetradrachms around 500 B.C. These coins outlived the Athenian state itself, remaining in circulation until around 300 A.D. Athenian currency dominated Mediterranean trade, and their coins have been found as far away as India[5].

The Romans, inspired by their Greek neighbors, introduced the silver denarius in 211 BC and eventually standardized a tri-metallic system under Emperor Augustus in 23 B.C. Using gold, silver, and bronze, this system outlived the Roman Empire, with its coinage circulating in various forms well into the early Middle Ages, roughly up to 800 A.D[6][7]. This leads us out of antiquity, but by this point in time, precious metals had proven their ability to endure collapses of civilizations and still retain their value as units of exchange.

There were problems, however, as later Roman emperors debased the quality of these coins by mixing precious metals with cheaper alloys. Debasement led to inflation and a steady decline in purchasing power, and the population, accustomed to valuing coins by their metal content rather than by the decrees of emperors, grew confused as prices and coinage diverged. Another issue was the supply of precious metals themselves. Demand eventually outpaced what mines could produce, an issue that became particularly noticeable after the collapse of the Roman Empire. In the absence of reliable coinage, parts of Europe reverted to more primitive forms of currency, such as squirrel skins, or used land and other commodities as means of exchange.

By the 1200s, Europe had significantly lagged both economically and intellectually, compared to the Arab world. A key turning point began with Leonardo of Pisa, later known as Fibonacci. After studying mathematics in modern-day Algeria, Leo returned to Pisa and published his findings in his Liber Abaci. Most essentially, he introduced the Indo-Arabic numeral system, which greatly simplified the process of complex mathematical calculations, which were found to be extremely helpful in commercial applications. It cannot be overstated how essential this new system was for the beginnings of modern finance; suffice it to say that these numerals are used to this day in every field of human labor that requires math. This breakthrough spread quickly throughout Italy and eventually to the rest of Europe[8].

The Medicis in Florence used this system alongside strict bookkeeping practices to establish the first proper banks and monetary exchanges (critical on a continent with many different currencies) across Europe, greatly assisting in commercial development and becoming fantastically wealthy along the way[9]. The maritime Republic of Venice began experimenting with the first forms of shipping insurance, calculating rewards for investments in merchant ships, which always ran the risk of not returning to port after a voyage had begun. Venice was also responsible for the first war bonds, using them to fund a war against the Byzantine Empire with public funds[10]. The Knights Templar began implementing the predecessor to the “check” by allowing pilgrims to deposit gold before departure on the long and dangerous journey to the Holy Land (mitigating the risk of being robbed along the way), receiving a bill, and being able to withdraw gold in exchange for the bill once they finally arrived[11].

Just as religious leaders in Sumeria were interested in money, so too was the Catholic Church. During the height of the Middle Ages, the Church ruled its own country (the Papal State) and maintained a monopoly on religion in Europe. It waged wars against its neighbors in Italy and financed lavish constructions in Rome, which can be seen in Vatican City to this day. All of this required lots of money. The Church originally forbade the practice of usury (charging of interest), and workarounds were discovered to circumvent these restrictions and stay in the good graces of the Church[12]. Ultimately, the Church itself gave in by running up debts with Jewish merchants (who were excluded from Catholic laws on usury, a common workaround) and encouraging the development of loans in order to pay for the construction of St. Peter’s Basilica, an immensely expensive undertaking. The institution of indulgences (very basically, paying the Church for a ticket to heaven) helped secure funding and contributed greatly to shattering the unity of faith in Europe. Martin Luther’s 95 Theses were largely focused on grievances with the practice of indulgences. As Protestantism took root, especially in countries like the Netherlands, the conservative approach of the Church towards money was done away with, allowing financial innovation to grow without moral guardrails. This paragraph is a gross oversimplification of centuries of change within the Church, but it is not a coincidence that the emergence of radical changes in money began just as its spiritual and temporal authority eroded. The split in faith was politically formalized at the Peace of Westphalia in 1648.

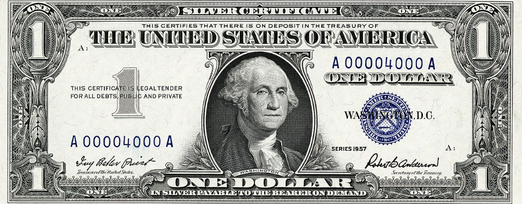

It was also around this time that the concept of money began to change. The demand for metals remained, but as mentioned before, they were not without flaws. A major issue was their safe transportation, an act that became dangerous if unsavory characters caught wind. Banknotes, bills of credit, and IOUs (I owe yous) were the first attempts to mitigate this. A person depositing at a bank received a bill acknowledging they were entitled to a set amount of gold, should they return, and it eventually became more convenient to exchange these bills with other people rather than return for the deposit of gold or silver. This became the basis of paper money, a fact which is attested to on U.S. dollar bills up to the year 1957! Compare it with a current one.

Note the writing under One Dollar

The 1600s and beyond were a huge century for the development of finance and money. In the previous century, the Spanish had discovered the largest, at the time, silver mine in the world at Potosi in Bolivia. Thanks to it, the Spanish were able to become the wealthiest and most powerful empire in Europe, yet despite having a seemingly endless supply of money, Spain went bankrupt 9 times between 1557 and 1666. Almost once a decade for a hundred years. Spain’s mismanagement of a veritable “mountain of money” is a topic that requires a book to explain, but the simple gist is that over spending on wars (the Eighty Years’ War against the Dutch among others), military over extension (the Empire spread over continents), poor accounting practices, internal economic mismanagement, and taking quick credit against future profits, can spell economic disaster[13]. There isn’t much to dwell on here, besides the fact that the most materially wealthy country in Europe somehow kept running out of money. This heralded the change that money, by this point in time, had become more than just silver and gold.

A key institution developed in the Netherlands worth mentioning is the Dutch East India Company (VOC), one of the first joint stock companies ever created in 1602. The VOC was one of the first chartered companies (giving birth to the modern corporation and arguably the first multinational corporation) and the first to be accessible to any Dutch citizen through the Amsterdam Stock Exchange, also one of the first modern stock exchanges[14]. The success of the VOC was explosive, and many countries were eager to imitate it, with varied results. The concepts of corporations and stock exchanges are now strongly linked to money, and the Dutch were the first to revolutionize these concepts, among many others. The VOC lasted until the Napoleonic Era, dissolved in 1799, but not before looting significant parts of Southeast Asia and greatly enriching shareholders.

Johan Palmstruch is a name most people are likely to be unfamiliar with, but he is best known for introducing paper money to Europe, as well as being responsible for one of the first documented cases of a bank run. Johan was born in Riga, trained in Amsterdam, and eventually convinced the King of Sweden to establish a bank under his leadership, after promising the King half the profits[15]. What separated the Stockholm Banco from older banks was the introduction of banknotes, which worked as certificates of deposit, and were attractive for many of the reasons mentioned above.

Two problems emerged with these that still plague banks to this day. As people became accustomed to using banknotes in exchange for goods in regular life, these bankers came across a devious realization. Most people do not return for their gold, preferring to keep it safe in a bank, so what if the bank started using its depositors' assets, keeping only enough to pay out the few that withdraw their gold? Customers eventually caught on, and to this day, banks still use depositors' money, but at least pay interest for the privilege. This trick was risky as a run could collapse the bank, but thanks to fractional reserve banking, the risk exists in some form to this day. The worst realization was that the bank could simply print more banknotes than it had gold in deposits, essentially creating money out of thin air. So long as clients never realized, Johan was able to perform one of the first feats of financial alchemy, turning paper into gold. Johan, however, made the mistake of getting greedy. It took only three years, from 1661 when the bank began printing banknotes to 1664, for this scheme to collapse, and a run ruined the bank[16]. Johan was sentenced to death in 1668, pardoned, served only two years for his crimes, and died a year after his release in 1671. The man may have died a failure, but his introduction of banknotes changed money forever.

It’s worth briefly mentioning one more financial alchemist, whose schemes of turning paper into gold caused substantially more damage than Johan ever did. John Law was a Scotsman, a gambler, and a man fascinated with the success of the Dutch VOC & Amsterdam Stock Exchange, after witnessing it firsthand during his residency there. His rise to prominence in the French court is a tale of its own, but Law managed to convince the Duke of Orleans, Regent of France, to appoint him as director of the Mississippi Company in 1717, intending to compete with the VOC. Not only did he eventually gain control of every other chartered company in France under him, but he also managed to gain exclusive control over “farming” the taxes of France, in addition to other revenue streams. Ever the gambler, Law pressed his luck and even managed to establish a bank in Paris on behalf of the King, which had been created with the intention of monetary reform. The crucial distinction with this bank was that, thanks to the autocratic support of the king, Law was eventually even able to declare banknotes as legal tender, equal to gold. This was only a temporary decree as popular backlash forced the king to rescind the order, but for the first time in history, paper money, with the assent of an absolute king, was deemed to have intrinsic value on its own! Law attempted to use his influence over France’s economy to enrich himself, largely by growing the Mississippi Company bubble. These schemes began to unravel as the Company consistently failed to generate profits, especially after the colonization of New Orleans (named in honor of the Duke of Orleans) failed, shareholders demanded their money back, and inflation triggered by the banknote decree began to ravage the French economy. It took only three years for the bubble to burst in 1720, and Law was forced to escape France, dying in Venice, impoverished, nine years later. France never truly recovered from the Mississippi Bubble bursting. Future monetary reforms were not attempted, and decades of continued economic stagnation eventually played a role in the French Revolution of 1789. Law’s schemes failed, but he was a trailblazer in the development of fiat money[17].

The introduction of fiat money into the world is worth taking a moment to appreciate, as it remains with us. A simple definition of fiat money is any government-issued currency that is not backed by gold, silver, or any type of commodity or asset. The value of the currency relies solely on the trust and authority of the issuing government. It only took a couple of centuries for the vast majority of the world to abandon precious metals as a basis for money. Muammar Gaddafi[18], former dictator of Libya, planned a gold-backed currency for oil-producing nations, though these plans were foiled after a revolution and an international coalition toppled his government. Zimbabwe, as of 2024, returned to a gold standard, becoming the first country of the 21st century[19]. Considering the hyperinflation the country has been suffering for years, this is no great surprise. In the interest of time, special attention will be given to the spread of fiat money in America, as that country would ultimately be the most responsible for the “new financial order” following WWII, and established the financial system of the world that more or less exists to the present.

It would take some time before fiat currency dominated the globe, but war turned out to be a significant factor in getting governments accustomed to it. To quote the great Cicero, “the sinews of war are infinite money”. Wars are expensive endeavors, always were and still are. When governments are fighting for their continued existence against foes, be they internal or external, concerns of providing national banks with enough gold to cover the deposits of citizens fall to the wayside. Gold is needed immediately to buy weapons, munitions, supplies, ships, bribes, salaries, and all the panoply of war. Under these circumstances, governments began to introduce fiat-based currency in times of emergency. The British first experimented with it during the Jacobite Rising of 1745, as well as during the Napoleonic Wars (1797-1821)[20]. A similar situation emerged in America during the Civil War (1861-1865). The Confederacy adopted a fiat currency from the outset, promising to pay people back after the war was won. As the hopes for a Confederate victory faded, trust evaporated, and the currency collapsed due to inflation towards the end of the war. The Union also adopted a fiat currency, known as the greenbacks, the value of which fluctuated wildly, especially in the early and uncertain years of the War. Greenbacks would remain in circulation after the end of the War and were eventually convertible to gold by 1878.

The Civil War was also the first time income taxes were introduced in the USA, to help fund the war, though thanks to their unpopularity and wartime justification, they were allowed to expire in 1873. Coincidentally, this same year, the Coinage Act of 1873 was passed, which effectively ended the bimetallic standard (both silver and gold standards co-existing)[21]. This is an underappreciated moment, as historically, silver has seen much more widespread use as money than gold, and gold standards were only introduced in the 18th century. The USA formally adopted the gold standard in 1900, and although silver coins still remained in circulation, the value of the dollar was no longer pegged to the value of silver.

By the dawn of the First World War (1914-1918), the world had largely moved over to the gold standard, but it would only be a couple of decades from this point before it, like the silver standard, became history. Many countries suspended their gold standards as war broke out, adopting fiat currency to help finance the Great War. The German Empire was one such state, but naval blockades, continued military setbacks, and inflation began to erode the value of the German mark throughout the war. After the war was concluded with the Treaty of Versailles, the country was also strapped down with heavy war reparations (payable in gold, not fiat), and so was unable to return to the gold standard. The Weimar government that replaced the German monarchy was forced to devalue the mark, and as the Allied powers refused to ease up on their demands, the value of the mark plunged. In 1917, during the war, five mark notes were still printed, by 1922, 10,000 note marks, by 1923, 50 billion note marks, and at the peak in 1924, 100 trillion note marks! Things got so bad that wheelbarrows of money were needed to buy a loaf of bread, and the wheelbarrows were worth more than the money itself. The government was forced to renominate the currency and return to a gold standard, which it did in 1924. This fiasco soured opinions on fiat currency around the world, but the Great Depression in 1929 would provide another opportunity for it to prove its worth.

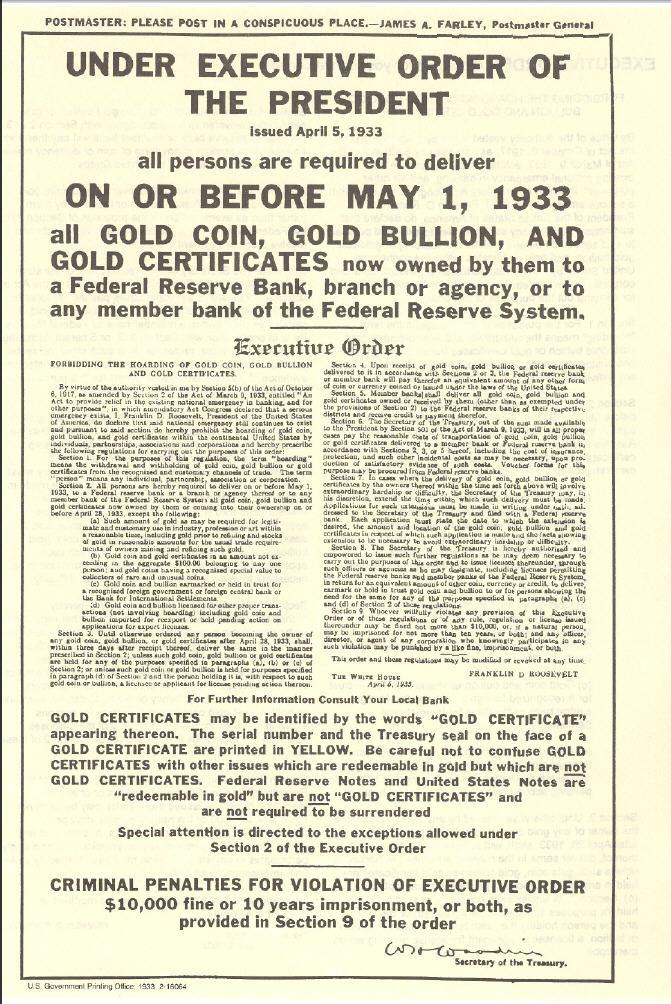

Without getting bogged down in details, one of the simple effects of the Depression was that gold (money) was hoarded, due to loss of jobs, most people had nothing to spend to revitalize the economy, and the government was forced to take action. Under President Franklin D. Roosevelt, the Gold Act of 1933[22] was passed, forbidding the hoarding of gold coins, ending the gold standard, and effectively making it illegal for private citizens to own any form of monetary gold. This act was extremely controversial (only repealed in 1975!) but officially used as an excuse to revitalize the economy and use fiat currency to expand the monetary supply, as well as fund government-sponsored projects to provide jobs. The dollar remained somewhat linked to silver and gold afterwards, but the Acts of 1873, 1933, and 1934 permanently severed these ties.

By the dawn of the Second World War (1939-1945), Britain had left the gold standard in 1931, France followed suit in 1936, and Italy never returned after leaving it when WW1 broke out back in 1914. Germany remained on the gold standard, though the Nazi party used a unique approach, allowing the Nazi government to greatly expand its monetary supply, which it used to rebuild its military. The Second World War was substantially different compared to the first, if only because it was fought to the bitter end. There was no uneasy ceasefire, and the Allied powers were able to dictate whatever terms they liked to the losing parties. By 1944, the outcome of the war was all but certain, and delegates from 44 different Allied countries met in Bretton Woods, New Hampshire, USA, to plan the future of the world economy out of the ashes. Institutions that last to the present day, like the International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (IBRD, today part of the World Bank) were created here. The USSR was the only country that refused to sign on, leaving the USA as the leading economic power outside of the communist world. The U.S. dollar became the cornerstone of this agreement, with the dollar becoming convertible to gold bullion for foreign governments and central banks. The trade-off here was that each country that agreed to the Bretton Woods system would guarantee the convertibility of its currency into dollars, allowing American banks and investors easy access into their economies[23].

The turn of the century in 1900 saw Europe effectively ruling the globe; the continent’s combined influence saw most of the globe under its sway. At the end of WWII, most of Europe lay in ruins and was unable to maintain its global empires. The United States was catapulted into a global superpower, and thanks to the Bretton Woods system, was allowed to invest in and rebuild countries that would have previously prevented it from gaining a foothold, especially in former European colonies. The good times were not meant to last forever, and as Europe began to rebuild and form closer economic unions in the 1950s and 1960s, cracks began to form in the system. Countries also began to worry about America’s deficit spending and concerns that America did not have enough gold to cover the huge volume of dollars they printed (sound familiar?), which led to countries liquidating their holdings of dollars in exchange for gold. In 1971, President Nixon officially ended the convertibility of dollars into gold, ending the Bretton Woods system and beginning the era that we live in today[24], where fiat reigns supreme. As a testament to how little trust there was towards the US and the Bretton Woods system, just days before Nixon made his announcement, the French deployed a battleship to withdraw the remainder of their gold reserves held at the Federal Reserve[25]. They had already withdrawn around 3,000 tons of gold in the years prior. In 1973, six members of the European Economic Community agreed to tie their currencies together and float them alongside the U.S. dollar. No further attempts were made to return the world to a gold standard; the value of money was placed in the trust of governments. Precious metals and their use as money were now a subject of history.

In the decade preceding this, the American government had already taken a few steps to end domestic ties with precious metals. In 1963, President Kennedy signed Executive Order 11110, a step in his plan to eliminate silver certificates in exchange for using Federal Reserve notes (modern dollars)[26]. Officially, this was done because the U.S. Treasury struggled to bid for the silver necessary for the minting of coins, due to greatly increased competition from industrial bidders (as it had seen new use in electronics manufacturing). In 1964, redemption of silver dollars was halted, and it was also the last year silver currency was ever minted. In 1968, any redemption of silver bullion was stopped, and by the 1970s, the remaining U.S. silver held in vaults was sold off to the public.

Now that fiat currency had officially supplanted the use of metals, explosive advancements in technology would bring dollars into the digital era. In the 1960s and 1970s, banks began establishing the Automated Clearing House (ACH), which began with the intention of speeding up the process of delivering paper checks to military personnel on time. A big innovation that helped spread ACH adoption among banks was enabling bank customers to receive Social Security checks through direct deposit, straight to their accounts, rather than having to deal with mailed checks, in 1975. In 1978, it became possible to electronically transfer money between accounts. With the advent of the internet, online payments became possible in 2001. Every single US Bank now belongs to the ACH system, and just about any type of payment or transfer, be it consumer, business, or government, can be handled on the ACH system[27]. Tens of trillions of dollars are transferred over the network every year, and it continues to serve as the backbone of digitizing the dollar. Other events that greatly contributed to the digital dollar include the creation of digital bank accounts and ATMs in the 1960s, in 1966, the New York Stock Exchange (NYSE) transitioned to a fully computerized system[28], and in 1971, the NASDAQ launched the ability for stock market trades to take place digitally. Today, about 60% of all stock market trading is attributable to high-frequency, automated trading, basically run by computer algorithms.

It is difficult to say whether these innovations in money are good or bad, but it cannot be ignored that they have evolved tremendously. Modern money is not without its faults; inflation is a feature, not a bug (compare the US rate of inflation since it left the gold standard[29]). The creation/printing and distribution of fiat money is extremely centralized, and those closest to the faucet are in the greatest positions to take advantage of it. Intrinsically, paper money really is worth nothing, and poor government policies are usually reflected in currency value drops. Fiat currency is hailed by many economists as a vast improvement over metallic standards of currency, and in many ways this is true. That said, fiat has many critics, mainly coming from believers in the old standard of money or those who believe in the new, like Bitcoin, which is considered by some as a welcome alternative to fiat. Bitcoin has its own troubles, but that is a different discussion. As we look into the future, the trend of digital currency seems like it is here to stay. The U.S. Federal Reserve announced that it has begun a pilot using Central Bank Digital Currency (CBDC)[30], which could see even physical paper notes become a thing of the past. Many other countries are also exploring and researching blockchain technology[31], and, ironically, it would seem like cryptocurrencies have become an excellent model for governments to imitate. Now that newer generations of people are more familiar with technology and almost every member of the first world has their own smartphone, it wouldn’t be much of a stretch to see cash completely phased out. Most people don’t even use it in their day-to-day lives, and plenty of businesses operate entirely without it. Whether or not this is a good thing for the average individual is a separate issue; banks and governments will do what is most expedient, as they have always done.

This is a bare bones outline on the creation of money and provides only the essentials of where it started up to how it got to the modern day. There is far more to say about this topic, but it must be kept short. There are plenty of other institutions and individuals who greatly contributed to the advancement of money that were, sadly, omitted here, but it is hoped that this article serves as a good primer or jumping-off point for additional research.

[1] https://www.zmescience.com/science/news-science/origins-of-writing-kish-tablet-5500-years/

[2] Ascent of Money, Ferguson, pg. 29-31

[3] https://www.thearchaeologist.org/blog/the-role-of-the-lydians-in-the-invention-of-coinage

[4] https://visit.varna.bg/en/varna_oldest_gold_treasure_in_the_world.html

[5] https://worldhistoryedu.com/tetradrachm-origin-story-weight-standards-and-significance/

[6] https://romanempiretimes.com/roman-coins-and-the-monetary-system-of-the-roman-empire/

[7] Ascent of Money, Ferguson, pg. 25

[8] Ascent of Money, Ferguson, pg. 33

[9] Ascent of Money, Ferguson, pg. 46

[10] https://academic.oup.com/book/52333/chapter-abstract/421095447?redirectedFrom=fulltext

[11] https://www.bbc.com/news/business-38499883

[12] Ascent of Money, Ferguson, pg. 37

[13] https://mises.org/mises-wire/three-centuries-boom-bust-spain

[14] https://www.britannica.com/topic/Dutch-East-India-Company

[15] https://www.riksbank.se/en-gb/about-the-riksbank/history/historical-timeline/1600-1699/sveriges-riksbank-is-founded/

[16] https://en.wikipedia.org/wiki/List_of_bank_runs

[17] Ascent of Money, Ferguson, pg. 128, 138-158

[18] https://www.cgaa.org/article/gaddafi-gold-dinar

[19] https://www.forbes.com/sites/nathanlewis/2024/04/09/zimbabwes-central-bank-starts-africas-path-to-a-gold-standard/

[20] https://www.jstor.org/stable/2122576

[21] https://www.usmint.gov/news/inside-the-mint/mint-history-crime-of-1873

[22] https://www.presidency.ucsb.edu/documents/executive-order-6102-forbidding-the-hoarding-gold-coin-gold-bullion-and-gold-certificates

[23] https://www.investopedia.com/terms/b/brettonwoodsagreement.asp

[24] https://history.state.gov/milestones/1969-1976/nixon-shock

[25] https://www.helleniscope.com/2025/07/31/august-1971-the-day-a-french-warship-came-to-new-york-to-repatriate-french-gold/

[26] https://www.armstrongeconomics.com/research/a-brief-history-of-paper-money/executive-order-11110-end-of-silver-coinage/

[27] https://www.federalreservehistory.org/essays/automated-clearing-house

[28] https://finance.yahoo.com/news/day-market-history-nyse-gets-155601598.html

[29] https://www.investopedia.com/inflation-rate-by-year-7253832

[30] https://www.federalreserve.gov/central-bank-digital-currency.htm

[31] https://cbdctracker.org/